Strengthening the U.S. Retirement System Requires Recognizing and Addressing Demographic Disparities

LOS ANGELES – December 15, 2023 – Fewer than one in four Americans (24%) strongly agree they are currently building or have built a large enough retirement nest egg. However, this sentiment varies dramatically across demographic segments, according to A Compendium of Demographic Influences on Retirement Security (“Compendium”), a comprehensive survey report released today by nonprofit Transamerica Center for Retirement Studies® (TCRS) in collaboration with Transamerica Institute®.

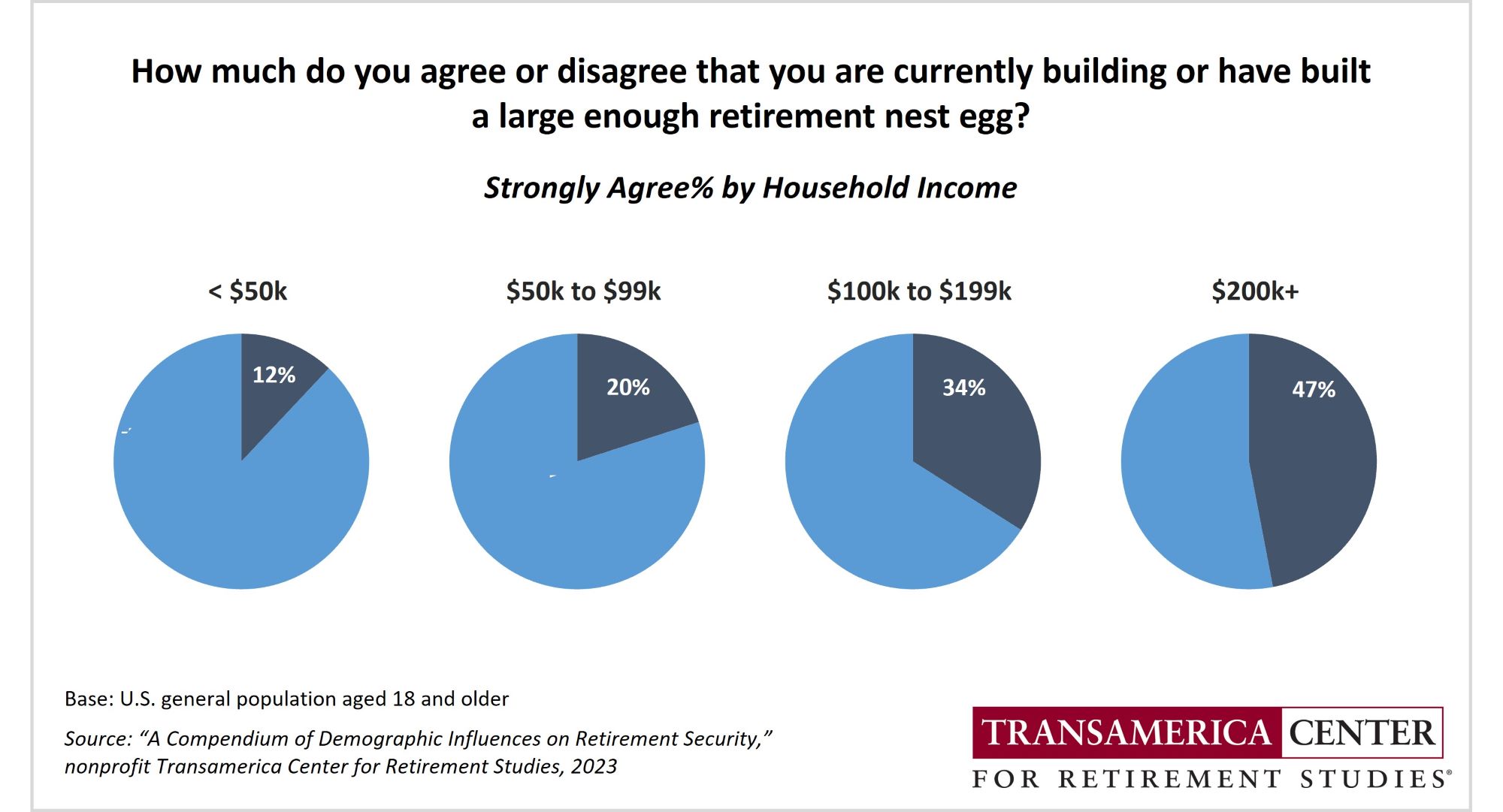

Just 12% of individuals with a household income (HHI) of less than $50,000 strongly agree they are currently building or have built a large enough retirement nest egg, compared with 20% of those with an HHI of $50,000 to $99,999, 34% with an HHI of $100,000 to $199,999, and 47% with an HHI of $200,000+.

“Demographic influences can profoundly affect an individual’s and family’s ability to prepare for a financially secure retirement. A greater understanding of these influences can help policymakers, the retirement industry, and employers to identify opportunities, envision solutions, and inform priorities for strengthening our retirement system,” said Catherine Collinson, CEO and president of Transamerica Institute and TCRS.

As part of TCRS’ 23rd Annual Retirement Survey, one of the largest and longest-running surveys of its kind, the Compendium is based on a survey of the U.S. general population aged 18 and older. It offers more than 25 indicators of retirement readiness by household income, urbanicity, race/ethnicity, gender, and LGBTQ+ status.

Retirement Readiness Increases Dramatically With Household Income

“A person’s ability to financially prepare for retirement is greatly impacted by their household income. Lower income earners have fewer funds available to save and, moreover, they have less access to employer-sponsored benefits that can help them save, invest, and protect their savings. As a result, they often end up relying on Social Security to fund their retirement,” said Collinson.

- Fifty-two percent of individuals with an HHI of less than $50,000 rely or expect to rely primarily on Social Security in retirement, compared with 34% of those with an HHI of $50,000 to $99,999, 20% with an HHI of $100,000 to $199,999, and nine percent with an HHI of $200,000+.

- Retirement savings dramatically increase with household income. Among those not yet retired, individuals with an HHI of less than $50,000 have saved just $1,000 in total household retirement accounts. In contrast, those with an HHI of $50,000 to $99,999 have saved $36,000, those with an HHI of $100,000 to $199,999 have saved $156,000, and those with an HHI of $200,000+ have saved $609,000 (estimated medians).

- Only 59% of employed workers with an HHI of less than $50,000 are offered a 401(k) or similar plan by their employer, and 59% of them participate. In comparison, 74% of those with an HHI of $50,000 to $99,999 are offered a plan, and 76% participate. Eighty-four percent with an HHI of $100,000 to $199,999 are offered a plan, and 86% participate. Eighty-four percent of employed workers with an HHI of $200,000+ are offered a plan, and 95% participate.

- Among those who have not yet retired, 52% percent of individuals with an HHI of less than $50,000 and 44% of those with an HHI of $50,000 to $99,999 expect to retire at age 70 or older or do not plan to retire, compared with 32% of those with an HHI of $100,000 to $199,000 and 30% with an HHI of $200,000+.

The Saver’s Credit is an IRS tax credit to promote retirement savings among low- to moderate-income individuals saving in a 401(k) or similar plan or IRA. Fewer than four in 10 Americans who potentially meet the tax credit’s income eligibility requirements are aware of it.

Rural Residents Are Getting Left Behind

“Economic activity in the U.S. has become concentrated in urban and suburban areas in recent decades. As a result, rural residents have been left behind in many ways, including retirement readiness,” said Collinson.

- Only 17% of rural residents are very confident they will be able to fully retire with a comfortable lifestyle, compared with 20% of suburban and 27% of urban residents.

- Rural residents have lower household incomes than urban and suburban residents ($50,000, $66,000,

- $82,000, respectively) (estimated medians).

- More than four in 10 rural residents (41%) rely or expect to rely on Social Security as their primary source of income in retirement, compared with just 30% of both suburban and urban residents.

- Among those who are not yet retired, rural residents have saved $7,000 in total household retirement accounts, while urban residents have saved $50,000 and suburban residents have saved $67,000 (estimated medians).

- Only 67% of employed rural workers are offered a 401(k) or similar plan by their employer, and 72% of them participate. In comparison, 77% of both suburban and urban workers are offered a plan, and approximately eight in 10 participate (81%, 80%, respectively).

- Almost half of rural residents (48%) who are not yet retired expect to retire at age 70 or older or do not plan to retire, compared with 40% of both suburban and urban residents.

Influences of Race and Ethnicity on Retirement Readiness

“The U.S. population is becoming increasingly diverse, especially among younger generations. This trend is reflected in the survey’s findings across race and ethnicity. The findings identify commonalities, expose disparities, and raise questions for further research,” said Collinson.

- AAPI people report the highest household income at $99,000, followed by White ($77,000), Hispanic ($56,000), and Black people ($50,000) (estimated medians).

- Black (37%) and White people (34%) are more likely to rely or expect to rely on Social Security as their primary source of retirement income than Hispanic (28%) and AAPI people (19%).

- Among those who are not yet retired, AAPI people have saved $74,000 in total household retirement accounts while White have saved $60,000, Hispanic have saved $29,000, and Black people have saved $17,000 (estimated medians).

- Approximately seven in 10 people who are not yet retired share concerns that Social Security will not be there for them when they retire including Hispanic (75%), White (72%), AAPI (70%), and Black people (67%).

- Among employed workers, Black (78%) and White workers (76%) are generally more likely than Hispanic (72%) and AAPI workers (71%) to be offered a 401(k) or similar plan by their employer. However, among those offered a plan, Black workers (74%) are less likely than White (81%), Hispanic (79%), and AAPI workers (82%) to participate in the plan.

- Many people who are not yet retired expect to retire after age 70 or do not plan to retire including Hispanic (43%), White (42%), Black (39%), and AAPI (35%).

Women Face Greater Retirement-Related Risks Than Men

“Women are at greater risk than men of not achieving a secure retirement. For women, the persistency of the gender pay gap, limited access to employer benefits, and time out of the workforce for parenting and caregiving often translates to lower retirement savings and fewer government benefits,” said Collinson.

- Women report a total household income of $59,000 which is substantially less than the $82,000 reported by men (estimated medians).

- Fifty-two percent of women are employed or self-employed compared with 67% of men.

- Forty-seven percent of women have trouble making ends meet, compared with 39% of men.

- Almost four in 10 women (38%) rely or expect to rely on Social Security as their primary source of retirement income, compared with 26% of men.

- Women who are not yet retired have saved $21,000 in total household retirement accounts, an amount which is much less than the $73,000 saved by men (estimated medians).

- Among employed workers, women are less likely than men to be offered a 401(k) or similar plan by their employers (71%, 79%, respectively). And, among them, women are less likely than men to participate in it (76%, 82%, respectively).

- Forty-four percent of women and 38% of men expect to retire at age 70 or older or do not plan to retire.

An Improving Retirement Outlook for the LGBTQ+ Community

“Historically, the LGBTQ+ community has been a demographic segment at greater risk of retiring in poverty. In recent decades, however, the LGBTQ+ community has made great progress with the enactment of legal protections and recognition of rights. Importantly, the legalization of same-sex marriage makes same-sex spouses eligible for government and employer-sponsored retirement benefits,” said Collinson. “Today’s LGBTQ+ community has a more favorable retirement outlook than prior generations, but they still face headwinds.”

- Many LGBTQ+ people are early in their careers, have more junior-level jobs, and are just getting started with retirement savings. Many experienced employment-related setbacks during the pandemic.

- Survey respondents self-identifying as LGBTQ+ are much younger than non-LGBTQ+ (age 33, age 48, respectively) (medians).

- LGBTQ+ people have a total household income of $59,000 while non-LGBTQ+ report having $71,000 (estimated medians). LGBTQ+ are less likely than non-LGBTQ+ to be married or living with a partner (38%, 54%, respectively).

- Thirty-five percent of the LGBTQ+ and 31% of non-LGBTQ+ people indicate their financial situation has worsened since the pandemic began.

- LGBTQ+ and non-LGBTQ+ people are similarly like to rely or expect to rely on Social Security as their primary source of retirement income (30%, 33%, respectively).

- Among those who are not yet retired, the LGBTQ+ have saved just $14,000 in total household retirement accounts, an amount which is almost one-third of the $51,000 saved by non-LGBTQ+ (estimated medians).

- Employed LGBTQ+ workers are less likely than non-LGBTQ+ workers to be offered a 401(k) or similar plan by their employers (70%, 76%, respectively) in part due to their occupations. Among those who are offered a plan, LGBTQ+ workers are less likely than non-LGBTQ+ workers to participate in the plan (69%, 81%, respectively).

- Forty-seven percent the LGBTQ+ and 40% of non-LGBTQ+ people expect to retire at age 70 or older or do not plan to retire.

“Strengthening the U.S. retirement system requires addressing Social Security’s funding shortfalls and reinforcing social safety nets. It also requires a collective effort among policy makers and key stakeholders to ensure that workers have access to meaningful employment throughout their working years, expand retirement plan coverage so that all working Americans have the ability to save in the workplace,” said Collinson. “By increasing our understanding of demographic influences, we can more effectively address inequalities and implement equitable solutions for all.”

About Transamerica Center for Retirement Studies

Transamerica Center for Retirement Studies® (TCRS) is a division of Transamerica Institute®, a nonprofit, private foundation. Transamerica Institute is funded by contributions from Transamerica Life Insurance Company and its affiliates. TCRS and its representatives cannot give ERISA, tax, investment, or legal advice. This material is provided for informational purposes only and should not be construed as ERISA, tax, investment, or legal advice. Interested parties must consult and rely solely upon their independent advisors regarding their situation and the concepts presented here. For more information, visit www.transamericainstitute.org.

About the 23rd Annual Transamerica Retirement Survey

A 22-minute online survey was conducted within the U.S. by The Harris Poll on behalf of Transamerica Institute and TCRS between November 8 and December 13, 2022 among a nationally representative sample of 10,015 adults aged 18 and older. Data was statistically weighted where necessary for age by gender, race and ethnicity, region, education, marital status, household size, household income and propensity to be online to being them in line with their actual proportions in the population. Respondents were selected from among those who have agreed to participate in our surveys. The sampling precision of Harris online surveys is measured by using a Bayesian credible interval and the worker sample data is accurate to within +1.3 percentage points using a 95% confidence level. This credible interval will be wider among subsets of the surveyed population of interest. Percentages are rounded to the nearest whole percent.

3282225 12/23