Retirement Security Across Generations Is Faltering in the Post-Pandemic Environment

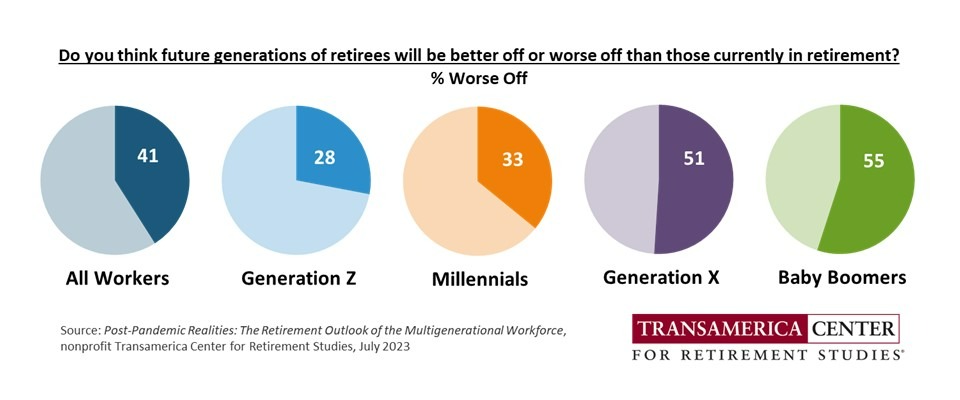

LOS ANGELES – July 6, 2023 – Forty-one percent of workers think that future generations of retirees will be

worse off than those currently in retirement, according to Post-Pandemic Realities: The Retirement Outlook of

the Multigenerational Workforce, a new survey report released by nonprofit Transamerica Center for

Retirement Studies® (TCRS) in collaboration with Transamerica Institute®. “The pandemic and turbulent economy have taken a toll on workers’ employment, finances, and retirement

preparations. Without additional support from policymakers and employers, it will be extremely difficult for

many workers to recover,” said Catherine Collinson, CEO and president of Transamerica Institute and TCRS.

“The pandemic and turbulent economy have taken a toll on workers’ employment, finances, and retirement

preparations. Without additional support from policymakers and employers, it will be extremely difficult for

many workers to recover,” said Catherine Collinson, CEO and president of Transamerica Institute and TCRS.

As part of TCRS’ 23rd Annual Retirement Survey, one of the largest and longest-running surveys of its kind, the study examines the employment, personal finances, and retirement preparations of U.S. workers aged 18 and older and employed by for-profit companies. The report provides comparisons of Generation Z, Millennials, Generation X, and Baby Boomers, and it offers recommendations for workers, employers, and policymakers.

Generation Z (Born 1997 to 2012)

“Generation Z began entering the workforce shortly before the pandemic. They are enduring the worst of the tumultuous labor market. Many have endured employment-related setbacks that negatively impacted their current situation and that could have repercussions for their long-term retirement prospects,” said Collinson.

- More than half of Generation Z workers (52%) experienced one or more negative employment impacts as a result of the pandemic ranging from layoffs and furloughs to reductions in hours and pay. Forty-two percent became unemployed at some point during the pandemic for various reasons.

- Almost six in 10 Generation Z workers (57%) have trouble making ends meet. Thirty percent currently have two or more jobs and 57% have a side hustle.

- Generation Z workers’ current financial priorities include paying off debt (50%), just getting by to cover basic living expenses (47%), building emergency savings (38%), and saving for retirement (35%). Twenty-one percent cite supporting their parents as a financial priority.

- Despite these competing priorities, two-thirds of Generation Z workers (66%) are saving for retirement through a 401(k) or similar plans and/or outside the workplace – and they started saving at age 19 (median). Those participating in a 401(k) or similar plan contribute 20 percent (median) of their annual pay.

- Generation Z workers have saved $29,000 (estimated median) in total household retirement accounts and only $1,000 (median) in emergency savings. An alarming percentage (28%) have dipped into their retirement savings by taking a hardship withdrawal or early withdrawal from a 401(k) or similar plan or IRA.

“Generation Z workers are establishing themselves in the workforce and gaining access to employment, compensation, and benefits. They have a long time horizon to build and grow their retirement savings, especially if they can quickly recover from recent challenges. Staying focused and becoming even more resilient are key ingredients for their future success,” said Collinson.

Millennials (Born 1981 to 1996)

“Millennials entered the workforce around the Great Recession, which began in late 2007, and experienced a difficult economy early in their careers. Now, they are confronting pandemic-related setbacks while trying to manage work-life balance. Many are falling behind on their retirement savings,” said Collinson.

- Almost half of Millennial workers have trouble making ends meet (48%). More the one in five (22%) currently have two or more jobs and 45% have a side hustle.

- Millennial workers’ current financial priorities include paying off debt (60%), saving for retirement (52%), building emergency savings (46%), supporting children (44%), and supporting their parents (17%).

- Forty percent are currently serving and/or have served as a caregiver for a relative or friend during their career. Among them, almost nine in 10 (89%) made one or more adjustments to their employment ranging from missing days of work and reducing hours, to forgoing a promotion or quitting a job altogether.

- Seventy-eight percent of Millennial workers are saving for retirement in a 401(k) or similar plan and/or outside the workplace. They began saving at age 25 (median). Those participating in a 401(k) or similar plan contribute 12 percent (median) of their annual pay. • Millennial workers have saved $49,000 (estimated median) in total household retirement accounts and only $3,500 (median) in emergency savings. Almost one in four (24%) have dipped into their retirement savings by taking a hardship withdrawal or early withdrawal from a 401(k) or similar plan or IRA.

“Millennials are in their late twenties to early forties and currently living their ‘sandwich years’ of juggling employment, raising children, and caring for aging parents – circumstances that can greatly influence their ability to save and invest for retirement. It’s especially important for them to focus on planning,” said Collinson.

Generation X (Born 1965 to 1980)

“Generation X entered the workforce in the 1980s and 1990s as traditional pension plans started disappearing. At the time, 401(k) plans were just becoming available but relatively few workers had access and saved in them,” said Collinson. “Generation X now is in their forties and fifties, many have inadequately saved, and they seek to extend their working years beyond traditional retirement age.

- Only 17% of Generation X workers are very confident they will be able to fully retire with a comfortable lifestyle and just 24% “strongly agree” they are building a large enough retirement nest egg.

- Eighty-one percent of Generation X workers are saving for retirement in a 401(k) or similar plan and/or outside the workplace. They began saving at age 30 (median). Those participating in a 401(k) or similar plan contribute 10 percent (median) of their annual pay.

- Half of Generation X workers (50%) expect their primary source of retirement income to come from selffunded savings, including 401(k)s, 403(b)s, and IRAs (40%) or other savings and investments (10%). Twentysix percent expect to primarily rely on Social Security. Eighty percent are concerned that Social Security will not be there for them when they are ready to retire.

- Generation X workers have saved $82,000 (estimated median) in total household retirement accounts and only $5,000 in emergency savings. Nineteen percent have dipped into their retirement savings by taking a hardship withdrawal or early withdrawal.

- Forty percent expect to retire at age 70 or older or do not plan to retire, and 54% plan to work in retirement. However, only 57% are focused on staying healthy and just 46% are keeping their job skills up to date.

“For Generation X, retirement is a light in the distance that is growing closer and brighter. Now is the time for them to fully engage in financial planning, saving and investing, and be hypervigilant in safeguarding their health and employability so they can continue to work until they are ready to retire,” said Collinson.

Baby Boomers (Born 1946 to 1964)

“Baby Boomers are now in their late fifties to late seventies. They have rewritten societal rules at every stage in life, including retirement. They are working into older age and demonstrating that work and retirement are not mutually exclusive,” said Collinson. “Baby Boomers were already mid-career when 401(k) plans were introduced. They started saving at an older age compared with younger generations and have not enjoyed the same longterm time horizon to grow their investments.”

- Almost half of Baby Boomer workers (49%) expect to or already are working past age 70 or do not plan to retire. Their greatest retirement fears are outliving their savings and investments (49%), declining health that requires long-term care (43%), and that Social Security will be reduced or cease to exist in the future (40%).

- Forty-one percent of Baby Boomer workers expect Social Security to be their primary source of retirement income, while almost four in 10 (39%) expect to rely on income from 401(k)s, 403(b)s, and IRAs (28%) or other savings and investments (11%).

- Eighty-five percent of Baby Boomer workers are saving for retirement in an employer-sponsored 401(k) or similar plan and/or outside the workplace. They began saving at age 35 (median). Those participating in a 401(k) or similar plan contribute 10 percent (median) of their annual pay.

- Baby Boomer workers have saved $289,000 (estimated median) in total household retirement accounts and only $25,000 (median) in emergency savings. Twelve percent have taken a hardship withdrawal or early withdrawal from a 401(k) or similar plan or IRA.

- Only 34% have a backup plan for income if forced into retirement sooner than expected.

“Among those still in the workforce, Baby Boomers are especially vulnerable to employment setbacks, volatility in the financial markets, and increasing inflation – all of which could disrupt their retirement plans and with little or no ability to recover. It’s critically important they have contingency plans for the unexpected,” said Collinson.

“Urgent attention from policymakers, the private sector, and employers is needed to strengthen our retirement system so that workers of current and future generations can retire with dignity. The SECURE 2.0 Act of 2022 has a multitude of provisions that address many issues, but a highly coordinated effort is needed to ensure they are implemented and successful. Moreover, it is time to strengthen Social Security and Medicare and expand these benefits to include long-term care services, affordable housing, and improved financial literacy,” said Collinson

Post-Pandemic Realities: The Retirement Outlook of the Multigenerational Workforce provides detailed survey findings about Generation Z, Millennials, Generation X, and Baby Boomers. To download the report, visit www.transamericainstitute.org. Listen to our weekly podcast ClearPath – Your Roadmap to Health & WealthSM. Follow on LinkedIn, Facebook, and Twitter @TI_insights and @TCRStudies.

About Transamerica Center for Retirement Studies

Transamerica Center for Retirement Studies® (TCRS) is an operating division of Transamerica Institute®, a nonprofit, private foundation. Transamerica Institute is funded by contributions from Transamerica Life Insurance Company and its affiliates. TCRS and its representative cannot give ERISA, tax, investment, or legal advice. This material is provided for informational purposes only and should not be construed as ERISA, tax, investment, or legal advice. Interested parties must consult and rely solely upon their independent advisors regarding their situation and the concepts presented here. For more information about TCRS, please refer to www.transamericainstitute.org and follow TCRS on Twitter at @TCRStudies.

About the 23rd Annual Transamerica Retirement Survey

The analysis contained in Post-Pandemic Realities: The Retirement Outlook of the Multigenerational Workforce was prepared internally by the research team at Transamerica Institute and TCRS. A 22-minute online survey was conducted within the U.S. by The Harris Poll on behalf of Transamerica Institute and TCRS between November 8 and December 13, 2022 among a nationally representative sample of 5,725 U.S. adults age 18+, who work full- or part-time in a for-profit company employing one or more employees (“workers”). Data was weighted where necessary for age by gender, race/ethnicity, region, education, marital status, household size, household income and propensity to be online to being them in line with their actual proportions in the population. Respondents were selected from among those who have agreed to participate in our surveys. The sampling precision of Harris online polls is measured by using a Bayesian credible interval and the worker sample data is accurate to within +1.7 percentage points using a 95% confidence level. This credible interval will be wider among subsets of the surveyed population of interest. Percentages are rounded to the nearest whole percent.

2965908 07/23